by Melvyn Morrison

Our recent Risk Congress at the prestigious Plaza Theatre in Brussels, dedicated to the theme of ‘Countering Economic Crime towards 2023’, was the venue for expert opinions from a number of eminent speakers, including Michaël André, the Head of Enforcement at the Financial Services and Markets Authority (FSMA) in Belgium. The FSMA is an autonomous public institution that, together with the National Bank of Belgium (NBB), supervises the Belgian financial sector. For example, Michaël is responsible for the day-to-day and strategic management of the Enforcement department, and for spearheading the investigation process giving rise to possible sanctions (for all areas of supervision).

Risk & Compliance Platform Europe: “What is the mission of the FSMA in Belgium?”

Michaël: “As a supervisory authority in Belgium, the FSMA is responsible for:

– ensuring that the financial consumer is treated honestly and equitably;

– working towards the fair and orderly operation of the financial markets and for the transparency of these markets;

– promoting the proper provision of financial services by verifying compliance in accordance with the rules of conduct;

– supervising financial products, service providers and supplementary pensions; and

– contributing to improving the financial education of consumers.”

Risk & Compliance Platform Europe: “Can you briefly explain how the FSMA takes action in Belgium?”

Michaël: “When performing its supervisory tasks, the FSMA can take the following types of action:

– Contact point, information provision and dialogue: the FSMA can provide information and explain the prevailing rules in force to financial consumers as well as companies, institutions and persons under its supervision;

– Circulars, communications, recommendations and moratoria: these instruments can be used by the FSMA to explain and interpret the rules so that the relevant actors know how to implement the legislation;

– Corrective measures: the FSMA can impose various corrective measures. For example, if the FSMA decides that information is missing from a prospectus, it can compel the issuer to publish this information, or can publish additional information itself. The FSMA can also require changes to be made, e.g. to advertising materials for financial products;

– Inspections: the FSMA can request companies, institutions and persons under its supervision to provide the necessary documentation and information, and can also conduct on-site inspections in order to verify compliance with all of the rules;

– Warnings: Financial service providers who wish to offer their services in Belgium must first register with or receive authorization from the competent supervisory authority. If a financial services provider offers its services without registering or without receiving authorization, the FSMA publishes a warning to advise the public. This information is also reported to the judicial authorities;

– Suspension: the FSMA ensures that price-sensitive information relating to listed companies is available to everyone at the same time. If this is not the case, the FSMA can suspend trading in the shares until this information has been made available to everyone;

– Administrative measures: if the FSMA determines that a financial service provider no longer fulfils the conditions for registration or authorization, it can take administrative measures that, in the most severe form, can result in the financial services provider no longer being able to perform its activities;

– Administrative sanctions: the FSMA can impose fines or penalties for infringements of financial legislation.”

Risk & Compliance Platform Europe: “What is the primary mandate of the Enforcement department of the FSMA in Belgium?”

Michaël: “The primary mandate of the Enforcement department is to support and reinforce supervisory action taken by the FSMA. This is achieved by:

– ensuring that financial services and products cannot be offered to the public without appropriate supervision by the FSMA;

– contributing to a solid and effective sanctions procedure.”

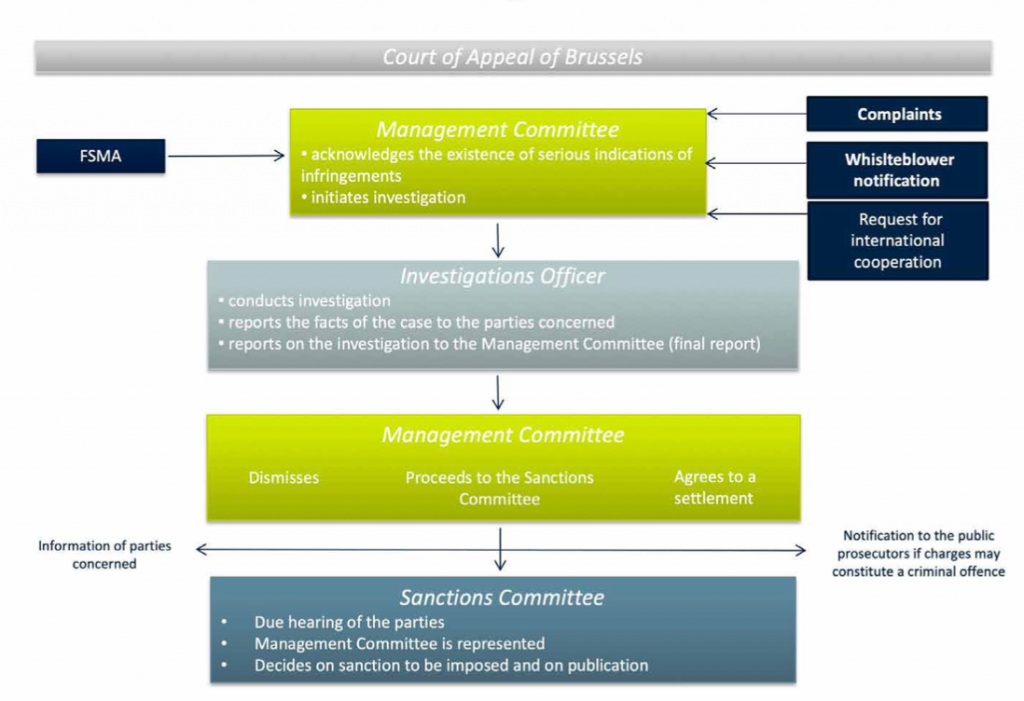

Risk & Compliance Platform Europe: “Can you briefly explain how the FSMA’ sanctions procedure is organized?”

Michaël: “The organization of FSMA’s sanctions procedure is outlined in Figure 1 below.”

Figure 1: Organization of the FSMA

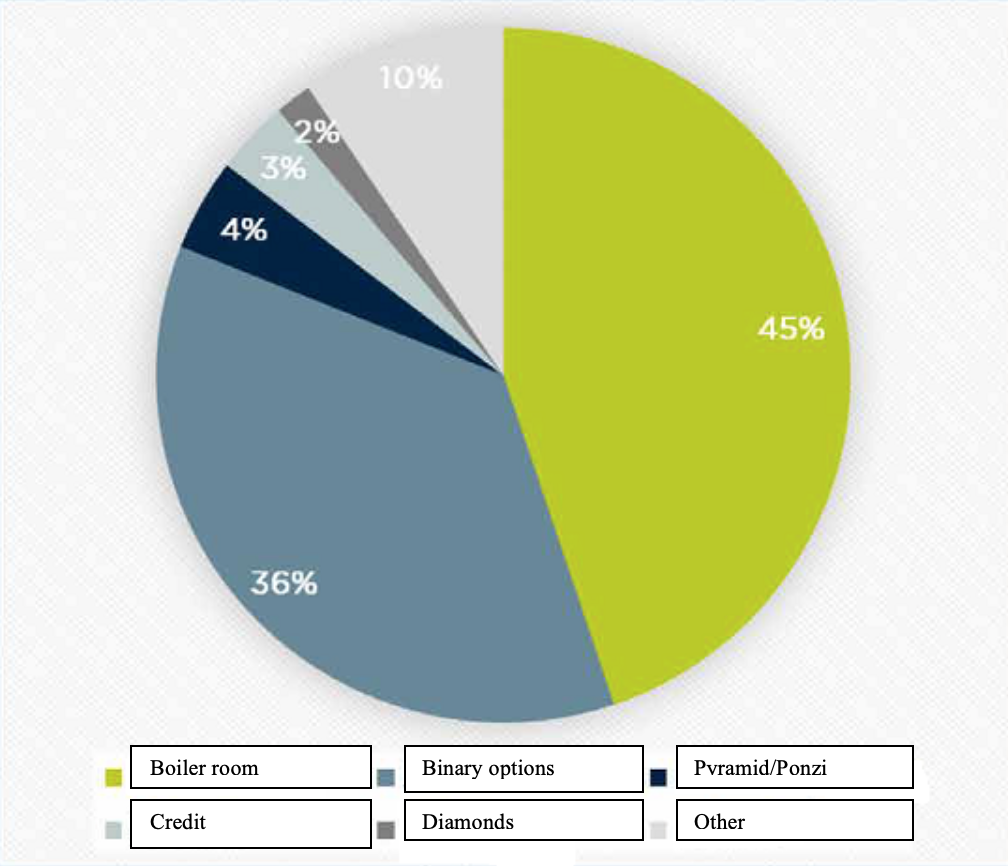

Risk & Compliance Platform Europe: “What do the warnings issued by the FSMA in 2017 relate to?”

Michaël: “A total of 116 warnings were issued in 2017. These warnings relate to the following categories:

– Boiler room: 52

– Binary options: 42

– Pyramid/Ponzi: 5

– Credit fraud: 4

– Diamonds fraud: 2

– Other: 11

The respective percentages for these warnings are shown below in Figure 2.”

Figure 2: Categories of warnings

Risk & Compliance Platform Europe: “How can a whistleblower contact the FSMA?”

Michaël: “A whistleblower is a person employed in the financial sector who observes and reports one or more infringements of the financial legislation (which the FSMA is responsible for enforcing). A whistleblower can use various channels to report an infringement, e.g. via the Whistleblowers’ point of contact section on the FSMA website (www.fsma.be), by phone, in writing, or at a face-to-face meeting. The FSMA guarantees that the identity of a whistleblower will be kept secret. Reports can also be made anonymously. The law protects persons who, in good faith, report an infringement to the FSMA. A whistleblower needs to describe the facts accurately and in detail so that the FSMA can conduct a thorough investigation. If possible, the facts should also be supported with documentary evidence.”

Risk & Compliance Platform Europe: “What can be concluded from the sanctions decisions already made by the FSMA?”

Michaël: “During the period from 2013 to date, the FSMA has made a total of 56 decisions (i.e. agreed settlements and decisions of the Sanctions Committee). For example, in 2017, 13 agreed settlements were published (e.g. relating to failure to submit documents for prior approval, infringement of the Prospectus Law, insider dealing, MiFID rules of conduct, etc.). In 2018, so far, the Sanctions Committee imposed sanctions in 4 cases, and 8 agreed settlements were also published (e.g. relating to infringement of the Prospectus Law, insider dealing, supplementary pensions regulation, etc.). From this, we can conclude that an agreed settlement has proven to be an effective instrument for settling proceedings relating to the various areas of supervision. Another important aspect is that all decisions are made public via the FSMA website. Finally, the sanction dossiers are increasingly linked to new areas of FSMA supervision (alongside market manipulation and insider dealing).”

Interactive Plenary Session: Michaël André, FSMA

24 December 2018