by Simon Lelieveldt

So what’s the deal with the ING 2018 attempt to raise the salary of Hamers? How should non-Dutchies understand the recent reprimand of former CEO Ralph Hamers, former supervisory board chair Jeroen van der Veer and some guy Breukink (former supervisory board member acting as the head of remuneration committee)? Quite a number of people are asking me to provide my perspective, and while I’ve documented quite a lot on this topic in the Dutch media (notable a range of articles at Follow the Money and an open youtube public lecture), I didn’t do so in English. But now that the disciplinary action and reprimand is final, it seems a good moment to try and explain the Dutch peculiarities and board dynamics ING to a wider international audience.

Inside story: details and big picture

I will tell you the inside story, as I see it. Because I was the ‘reporter’ as outlined in the rules for the Dutch Bankers Oath. I have triggered the case/reprimand by immediately reporting the announced pay raise (March 11, 2018, when not yet withdrawn by ING) as a violation of the Dutch bankers Oath and a host of other rules as well. As the former head of the Dutch Bankers Association department on bank supervision and financial markets I felt this my obligation. Although I must also add that for the first six months I chose to use a pseudonym.

No other board members at ING or financial institutions or bankers association joined me officially or formally, though some reached out to commend/back me on a personal basis. This informal board level support kept me on track/motivated during the five years between ING pay raise and final verdict.

Now let me warn you: the true compliance and legal details are pretty dense and complex. But that’s exactly why I felt it my obligation to raise the topic of misalignment with the bankers oath. It takes an insiders view to be able to pinpoint the numerous errors/law transgressions that had occurred. But I was also a bit afraid of going against unwritten informal norms to not call out higher level bank executives as the former bank association representative that I am.

However, when in August 2018 the Bankers Association published a position paper outlining that the Hamers-remuneration evasive trick was going to be the standard remuneration method in the Netherlands (thus formalising an evasive route by seeking a group of transgressors to make it look legal), I chose to disclose my true identity, which was reported in Follow the Money.

If you want the detailed tickets of the case and are happy to use translators and such, you can visit this google-drive with full background documentation on the case in all its details. It contains background information, a number of reports and research studies where I reconstruct the remuneration debate in the Netherlands since 2008 and relevant developments. I received a 9 out of 10 for this evaluation and reconstruction of relevant law, oath and contract terms that applied. And with that I obtained my degree as certified compliance officer.

Having done all this nitty-gritty footwork, I am open to professional challenges and discussions on the case at hand. But fact of the matter is that there are not too many lawyers/legal experts around that are also compliance professionals and that have also been present during board meetings and policy discussions on remunerations in the Netherlands. So feel free to disagree, but leave out cheap arguments/shots and bring your own tickets with you. There’s an ice berg of details in the Google-drive and I will try to outline below what it looks like.

March 2018: 50% pay raise using new idea of fixed shares

It all started with a carefully crafted pre-announcement of the planned Hamers pay raise via the local newspaper Financieele Dagblad. The FD from the reading of it, clearly got an informal heads-up, and were conned into describing the pay raise of ING for Hamers as innovative (and legal). The formal argument was that Hamers needed to be paid in line with the international top class management division that some thought he belonged to. And he was too much out of sync with the median income so, hell yeah, let’s make it up with a 50% pay rise in one year. But how? There is a variable remunerations cap in the Netherlands (self inflicted but also in law) that is in the way.

ING decided to introduce the concept of ‘fixed shares’ as a remuneration that would qualify as fixed pay (no caps on raising fixed pay) but in reality turns into variable remuneration as the fixed amount of money is used to buy shares ING which vary with exchange rates. Suffice to say that the clear evasion of remuneration rules for Hamers pay raise was dripping like mayonaise from French Fries.

It was also immediately clear to the public at large that someone was greedy at the top of ING and that ING-boards didn’t stop the greed. This all happened in spite of previous promises, rules, contracts and the social contract of ING with the public. So, although with a little bit of decency and common sense, the proposal should have been shelved after internal discussion, ING chose to pursue to seek the edges of reason and try the waters of the public opinion. That worked out nicely: a huge media backlash, customers fleeing the bank (doubling the bank switching numbers in 2018) and very negative political reaction.

So here we are, three days into the media row, and my challenge was: I want to call out all the board members (all supervisory/executive board members of ING) for their collective failure to not properly identify in advance the harm they would do to trust in banks by pursuing this remuneration proposal for Hamers. Not by doing a publicity stunt or being emotionally shocked and such (the typical political and media reaction) but just by using the law, the rules and the relevant agreements that ING had itself bought into. In fact, it was during Hamers seat in the Dutch Banking Association Board that all banks signed up to the bankers code and abide with it.

So that’s where it started. On Sunday evening March 11, I reported the ING board members violation to the Foundation that does the judgment on whether bank employees act according to the bankers Oath and the enshrined Code of Conduct. To me it was clear that the Supervisory Board and Executive Board of ING could have foreseen the public row but had wilfully chosen to shake the publics trust rather and try to give Hamers a raise, rather than respect the CRD rule 95.2 which states: ‘When preparing such decisions, the remuneration committee shall take into account the long-term interests of shareholders, investors and other stakeholders in the institution and the public interest.’

Ah, and I should mention that ING also subscribed to a gentlemen’s agreement on moderate remuneration in 2009 and was saved by government under terms which specified that they should not do funny or exuberant stuff in terms of pay raise. But ING quickly forgot those promises, so in 2011 that lead to the political reaction that companies with state aid cannot pay bonuses. ING then said sort of sorry and promised in its annual report 2011: ‘The board of Supervisors of ING wants to ensure that the topic of remuneration will never again become a topic of public debate.’

And even in 2017 they clearly were aware of the public interest dimension as their annual reports reads: ‘In determining executive remuneration, the ING Supervisory Board is aware of the public debate surrounding this topic and strives to balance all stakeholder interests. In this context, the Supervisory Board has decided to slightly increase the total (at target) remuneration of the CEO by 3% with effect from 1 January 2017.’

Despite these beautiful words, with ING so ostensibly not caring about public opinion I not only wrote a report to the disciplinary committee about the error to not take onboard the public interest. I also added my complaint as to the predictable unwillingness of ING to even want to discuss this topic under the Bankers Oath. My assessment was that ING board members felt like god-given do-gooders upon which everything was bestowed except the need to really comply with the Bankers Oath. That’s just for the people below in hierarchy. We, board members, of course only subscribe to it but no way that anyone dares to challenge us.

My final alinea of the report was thus directed at both ING and to the disciplinary board foundation (which after all, was being funded by bankers, so I had little trust in their objective rulings): “Bank employees can be expected to be prepared to submit to the disciplinary law. I assume that in practice your institute and Mr Hamers will not be willing, will be unable or will be too cowardly to deal with this complaint. That’s not the spirit of the Code of Conduct, but it is foreseeable. My complaint therefore already concerns the unwillingness of the entire Supervisory Board, ING management including Mr Hamers not to deal with this case under disciplinary law.”

Next 2 years: ING straight out sabotaged the processing of the filed report

In the two years that followed, ING indeed obstructed the processing of the complaint by claiming it was unfounded and throwing the kitchen sink of legal arguments in. Questions were asked in parliament (why is the complaint pending for more than a year now) and Ministry of Finance ducked the answer.

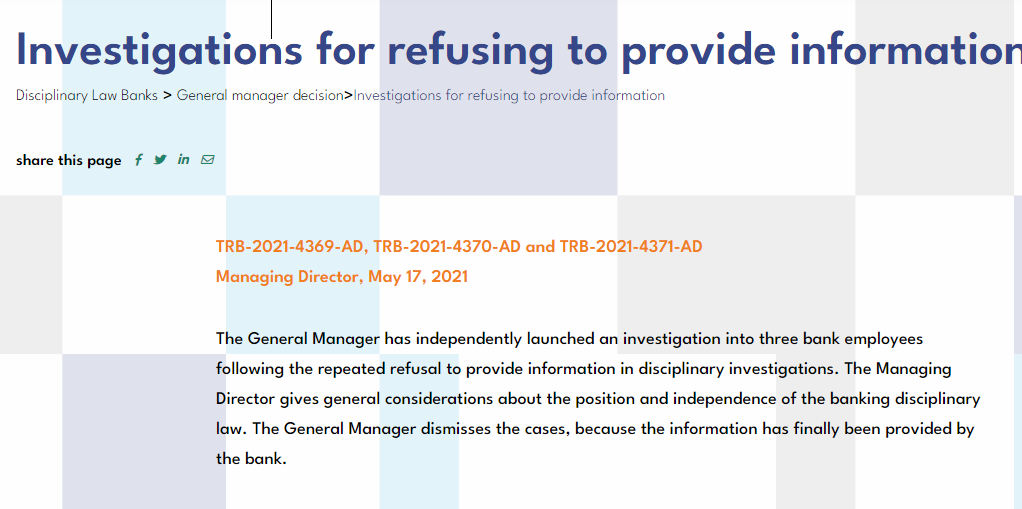

The foundation on disciplinary action then reverted to the strategy of sending in three new complaints of their own with respect to three senior officials of ING as they acted on instruction of their bosses to not cooperate with the processing of the complaint. Those three officials will have turned to their boss, I guess, saying: I may be facing disciplinary action because you do not wish to cooperate. I’m not going to be your fall guy. Deal with it yourself and cooperate.

Google-translation of decisions forcing ING to cooperate with investigation of pay raise under bankers oath

Above you see the mentioning of intermediary decisions of the bank oath disciplinary foundation/prosecutor where they drop the complaints for the three ING lower employees in exchange for full cooperation of ING on providing information about the pay raise.

But bottom line. This refusing to cooperate bought ING time to arrange an exit for Hamers without creating the image that UBS was getting in essence a not so super damaged goods executive known for not being able to be compliant with money laundering law.

Also do note that formally Hamers was the executive who explicitly directed ING to not fulfill its formal legal obligation to cooperate with every processing of bankers oath’s complaints (regardless of rank of employee). So I figured, that’s 1–0 for me. ING as an institution, Hamers and all board supervisory and executive members have not only ducked their responsibility on pay raise topics, they also actively prevented and blocked the bankers oath discussion and investigation on ethics and this will at least bear some weight along the line.

When looking at the current reprimands and verdict, you will not see a reference to this episode however. Because in the structure of the Bankers Oath disciplinary law, the reporter of a fact, is not the participant. A prosecutor is taking over the decision to follow up on a report and after that, it is up to the committees for complaints or committee for appeals to invite the reporter at their own initiative.

Of course, I repeatedly asked to be invited as the reporter-in-case to provide insights, facts, and regulatory analysis but while that was being turned down repetitively, I chose to document the whole process publicly. So that anyone interested in facts/history and arguments could check out the relevant reasoning in the case. And could see the omissions, errors of judgments in both my reasoning and that of the Commissions dealing with the case. In fact, it was the first open sourcing of a legal argument and regulatory discussion that I started.

Behind the scenes: internal dynamics at ING

In essence ING has had aggressive remuneration in 2009, right after bail out, and was curtailed. A gentlemen’s agreement between banks and government was agreed to stating ‘moderate remuneration’ as the norm. Nevertheless ING raised pay for executives too fast and too furious in 2011. Leading to new legislation prohibition bonus for state supported companies.

Then CEO Jan Hommen skipped logics as he promoted a snake oil type salesman Hamers to the board (jumping one level) to make ING up to date and aggressive commercially. Hamers had previously built a commercial empire but was sent to Germany (out of sight) as his aggressive selling was non-compliant with law. Having done his time in German ‘jail’ he was later on suddenly promoted by Jan Hommen in an idea to shake up the old bank.

Two logical CEO-successors, Leenaars and Van der Noordaa then left ING and ING fell for the fairy tale of digital Hamers who then continued his strategy of persona-building/image building and combined this with a Mao-like shake up of hierarchy to break the power of operations. In doing so ING lost sight/control of compliance and was unable to do any relevant monitoring of transactions. Leading to big fines along the way.

Now, president of supervisory board Van der Veer had promised Hamers big pay raises (as had Hommen) but this could only be done when ING was no longer on state support. In 2017 ING chose to give Hamers ‘only’ 5% raise, but in 2018 it was the last year of van der Veer as head of supervisory board. Incoming Hans Wijers had made it clear that he found the remunerations for Hamers bizar and he wouldn’t back them. So van der Veer and remuneration supervisory board member Breukink wanted to use 2018 as last chance to upgrade Hamers pay and they invented an anomaly like fixed shares (fixed pay in shares with a variable price: nice verbal invention but clear evasion of remuneration rules of EBA) to avoid the relevant EBA rules and the 20% bonus cap that banks had inflicted on themselves here in the Netherlands.

It can be assumed that when Dutch banks chose to agree to the banking code and new remuneration rules and bonus cap, they already had raising the fixed salary on their agenda as a plan-B move when they needed it. So the publicly stated bonus cap of banks was more a publicity stunt and the whole bankers oath in essence now looks like a publicity stunt. You can see this literally in the documents as ING argued in the discussion on the pay raise something along the lines of: ‘The bankers oath should only stress existing requirements, not create new ones’.

So the true board member dynamics are clear to everyone here in NL. ING and Hamers are greedy and will do anything including hurting the public trust to fill the pockets of Hamers. Bankers oath and rules are irrelevant. But this stings with normal people and bank employees who honestly make something out of the oath. And even a 5% pay raise in 2017 (when loads of ING personnel are being kicked out) is not something I think a normal board of supervisors should allow.

Dealing with the complaint: yes or no violation of the oath and law?

The exact argument on illegality of pay raise does not really matter much in my opinion as there are many ways that lead to Rome: either they violated evasion rules of EBA on remuneration or they forgot CRD rule 98.2 on balancing interests at stake during remuneration, or they violated the Dutch gentlemen’s agreement on moderate remuneration or the terms and conditions they subscribed to when receiving state aid or their internal morality/ethics principles. ING just wanted to give Hamers a raise and everything had to be bulldozered out of the way.

It is noteworthy to see that both the first complaints Commission and Appeals Commission in essence shove aside the EBA-regulations, relevant contract law and such to pretend as if the pay raise is acceptable in structure. The argument that it could misalign incentives and thus create the image of a conflict of interest for the top manager (as the pay shifts the interests to the shareholder perspective on each salary day) is not discussed/considered.

It’s pretty clear to me that they are afraid to put down in writing that the pay raise is illegal in letter and spirit and under the CRD requirements. Only by ignoring the whole rule set and agreements of the financial sector/ING and just limiting the scope to generic Dutch governance principles the suggestion can be maintained that in essence the pay raise structure is fine. I find that an indication for the desire of the appeals commission not to burn their hands too much (and be forced to issue a prohibition on execution of profession, which is what I asked for, for Hamers).

Approach and verdict of Commission of Appeal: clever and with clear merits but way too soft and ignorant

I wrote to the Commission of Appeal in August 2022 to ask; can you please invite me to the proceedings so I can share some further insights and help you orient and discuss the arguments. They turned the offer down. Instead they invited Hamers, Breukink and van der Veer, at the same time, to discuss the topic. But these three gentlemen declined to speak up and kept on claiming to be bound by confidentiality with respect to the topic of the pay raise.

This creates the interesting situation that ING, the sabotaging entity, is allowed to enter arguments into proceedings and leave out all relevant information at will. While someone like me, who is motivated, informed and can contribute with a certain intelligence to the proceedings and who could have been invited under the rules of the procedure, was not provided that opportunity. Leading the Commission of Appeal to not become aware of relevant additional facts of the case. I can only guess why. Perhaps they just didn’t want to hear the exact details of the case for fear of the conclusions that they would have to draw.

There are details such as: how ING probably never did any formal risk assessment on the pay raise/reputation impact, as required under financial law, how apart from HR-printing the desired pay raise outcome, no other functional staff was involved and how the culture of ING was that: you don’t mess with executives pay and you most certainly don’t speak up. That ING clearly forgot to read CRD4 amendment which added the obligation to check the public interest upon remuneration. That ING forgot the terms and conditions of its bail out agreements with the state. That ING sort of forgot the social contract it had with the public as well as the gentlemen’s agreement on moderated remuneration (subscribed to in 2009). That ING wilfully sabotaged the pay raise ethics complaint, is in the way in itself, a legal violation.

Having said that, the argument and reasoning of the Commission of Appeal still has merit. They have paved a way where board members and CEO’s of banks can no longer hide/exonerate all their activities under the reasoning: you cannot dispute my actions as a policy maker as I am establishing policy for the bank and policies are not to be disputed, only actual and concrete actions can be disputed. And that will certainly have an impact on board level responsibilities and actions.

Instead of turning to the previous visible sabotage of ING during the collection of information, the Commission created an interesting new setting, where they could see with their own eyes how three mature men, former board members, who all signed an oath to be open, transparant and reflective on their own actions and ethical impact, just didn’t want to tell them who was the first to suggest or agree that they would allow Ralph Hamers a big hand of cookies out of the cookie jar.

Reading the verdict and dynamics of the case treatment demonstrates an image of three school kids who do not want to snitch on each other. The Commission of Appeal says: it’s long ago, no need to still be silent. But they kept silent anyhow. The board room omerta is thus still stronger than the bankers oath. And interestingly, instead of slapping back with a full professional prohibition the three only get a reprimand. Now why is that? What could be happening?

I think the three muted gentlemen are so silent to protect the fourth actor in the play: Hans Wijers. Then commissioner Wijers was already on board as the incoming and foreseen supervisory board chairman. And in a strange paradox, the position of Wijers that he wasn’t going to cover as the supervisory board president for bizar pay raises, led to the momentum of an accelerated bizar pay raise under the leaving President van der Veer.

What Wijers should have done at that point in time is take his responsibility and veto the pay raise when it appeared ING was going to ignore public opinion, law and reason. But he kept calm, fell silent and let the public damage become a fact.

I can fully understand it, because the dilemma is if it would be good to interfere with a sitting supervisory board president that is well respected. Yet, the moral answer is: if you see a boat accident starting to happen, will you wait for the true captain to do something (when clearly he isn’t willing to) or will you act anyhow to preserve the ship, seeing that you are the new captain in a couple of weeks?

For this inaction, Wijers should thus be reprimanded just as much as the three reprimanded board members. But those three don’t want to spoil the beans on his involvement. Thus, they take the inevitable reprimand by the Appeals Commission on the chin, like a man. As if with this reprimand to only three people the story would end. But it doesn’t.

A wider approach: collective responsibility for all board members

Under Dutch law, each individual board member is responsible and liable for the actions of the collective. The basic idea is that at lower levels in the organisation you can specialise and say: It’s not my department. But at higher levels you have to look broader and take a holistic view. So when the CFO says A but as a non-involved Supervisory Board Member you still have reservations you either speak up if you see damaging consequences or become liable for agreeing with A. And that is what is at stake here.

If a group of formal policymakers/bestuurders sees an accident forthcoming and they are board members, how can some of the group hesitate, wait and do nothing by just pointing to the designated board member and their responsibilities? It’s a contradiction that doesn’t fit under our governance rules in the Netherlands.

The wider implications of the reprimands are that in fact all supervisory board members and all executive board members have silently stood by and said nothing, while knowing ING was going to run the remuneration truck into an innocent bystanding crowd of people fed up with greed in the bank sector. Under the logic of the Dutch civil law all ING supervisory and executive board member may thus consider themselves being reprimanded.

The merit of the approach of the Commission of Appeal is that it has made it abundantly clear that the classic legal and verbal defence lines of board members to not be judged under the Bankers Oath have been struck down. Policy responsibility as a board member still means being accountable for individual actions and possibly violating the oath.

All board members that were not part of the prosecutors complaint (but they were in my report, as I stressed the collective responsibility under article 2.9 of Dutch civil law) may thus have something to ponder. I would suggest they take this judgment to heart and understand it as a judgment of their lack of taking proper responsibility for the collective outcome.

6.37 The Appeals Committee has not found evidence of a serious and thorough investigation into the expectations of the various stakeholders and the social support to which they were bound under the 2015 Banking Code.

6.38 The insufficient care taken by the defendants with regard to the above aspects also resulted in a careful weighing of interests not being possible (Rule of Conduct 2). In the 2019 annual report, the Supervisory Board (with a changed composition) also expressed a critical view of its own actions in 2018 with regard to the remuneration proposal (see 2.33).

6.39 As a result, the defendants have culpably created a foreseeable risk that the proposal of a 50% salary increase would lead to such a commotion that society’s confidence in the bank was damaged (Rule of Conduct 7). The fact that the published proposal was withdrawn shortly afterwards does not detract from this. The unrest was — as acknowledged in the press release of 13 March 2018 (see 2.31) — already a fact.

Epilogue

There is always more to it and I can be wrong. But while all other actors shove around brief lines of communication which do not do justice to all the facts, rules and circumstances, I provide the tickets here and am open to be corrected. Just add the facts to my google drive and we will discuss.

In the mean time, the involved board members remain silent to honour a board room Omerta above the rule of law. They chose to drive a remuneration bus into the Dutch crowd all for the benefit of merely one, money laundering, CEO.

This is conduct that is gentlemen unbecoming. It’s disrespectful to all the people of ING that did and still do their best to honour the banking code in all respects, that are being trained and educated to do the best in the letter and spirit of the Banking Code.

If the gentle men Hamers, van der Veer en Breukink, as lower level members of any bank team would have behaved so rebellious and refuse cooperation during a report of a banking oath violation, they would have been kicked out and fired immediately for not complying with Wft-legal regulations that oblige cooperation in these matters. Why would treat them different now that they are board members?

The three reprimanded gentlemen can consider themselves lucky to have a Commission of Appeal that has chosen not to dive deeper into the legalities of the case and just provided a hand slap to make their point. But the message will fall deaf on their ears, for certain.

However, board members in the Financial Sector in the Netherlands may want to pay attention and wish to re-assess their responsibilities and actions more diligently, now that it is clear that there is no free pass for the Dutch Banking Oath on the board level.

PS. This case could not have been done without the tremendous efforts and endurance of the staff and prosecutor at ‘Tuchtrecht Banken’ that facilitates the processing of reports and the secretarial functions for the committees that deal with violations. I have come around to understand and highly appreciate the diligence and care with which they have maneuvered these complex waters. In fact, they are true heroes in this case, if you ask me.

The author, Simon Lelieveldt, is an Industrial Engineer active in the Dutch Banking and Payments sector. In his career, he has worked both as a bank supervisor and a banker in different roles such as project manager, consultant, senior policy-advisor interim-compliance manager and head of a department of professionals.