The European Supervisory Authorities (EBA, EIOPA, and ESMA – the ESAs) together with the European Central Bank (ECB), has recently released the results of the one-off “Fit-For-55” climate scenario analysis. Under the scenarios examined, transition risks alone are unlikely to threaten financial stability. However, when transition risks are combined with macroeconomic shocks, they can increase losses for financial institutions and may lead to disruptions. This calls for a coordinated policy approach to financing the green transition and the need for financial institutions to integrate climate risks into their risk management in a comprehensive and timely manner.

Objectives

The European Commission invited the ESAs and the ECB to assess the impact on the EU banking, investment fund, occupational pension fund and insurance sectors of three transition scenarios incorporating the implementation of the Fit-for-55 package, as well as the potential for contagion and amplification effects across the financial system.

The European Union’s Fit-for-55 package aims to stimulate investment and innovation in the transition to a green economy and plays a crucial role in the EU’s goal to achieve an emissions’ reduction of 55% by 2030 and climate neutrality by 2050. It aims to bring EU legislation in line with these goals with a set of policies that include – among others – the EU emissions trading system, the carbon border adjustment mechanism, sector-specific emissions targets, as well as revisions to the renewable energy and energy efficiency directive.

Scenarios and methodology

The climate stress test was conducted against three scenarios developed by the European Systemic Risk Board (ESRB), with the support of the ECB. The scenarios incorporate transition risks as well as macroeconomic factors, under the assumption that the Fit-for-55 package is implemented as planned.

- Under the baseline scenario, the Fit-for-55 package is implemented in an economic environment that reflects the ESCB’s June 2023 forecasts, while still facing additional cost related to the green transition.

- Under the first adverse scenario, transition risks materialise in the form of “Run-on-Brown” shocks, whereby investors shed assets of carbon-intensive firms. This hampers the green transition, since “brown” firms don’t have the financing they need to green their activities.

- Under the second adverse scenario, the “Run-on-Brown” shocks are amplified with other standard macro-financial stress factors

To measure the impact of the scenarios on the respective financial sectors (the so called “first round effects”), and to assess the potential for contagion and amplification effects across the financial system (the so called “second-round effects”), the ESAs and the ECB used top-down models. The estimates are produced relying on granular data and consider a time horizon of 8 years (from 2022 to 2030). The ESAs and the ECB models cover loans to Non-Financial Corporations (NFCs), equity, debt securities (including government bonds) and positions in funds held by a sample of financial institutions composed by 110 banks, 2,331 insurers, 629 institutions for occupational retirement provision (IORPs) and around 22,000 EU-domiciled funds.

Results

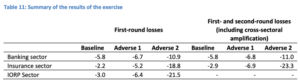

The results of the exercise show that estimated losses stemming from a “Run-on-Brown” scenario have a limited impact on the EU financial system. Over the 8-year horizon, total first-round losses stand between 5.2% and 6.7% of starting point exposures, in each sector. The second-round losses are mostly relevant for investment funds, and amount to 11.2% of starting point exposures.

The interaction of adverse macro-financial developments with transition risk factors could disrupt the evolving transition and substantially increase financial institutions’ losses, thereby impairing their financing capacity. This is assessed in the second adverse scenario where the “Run-on-Brown” shocks are coupled with adverse macroeconomic conditions. Under this scenario, the first-round losses registered by banks, insurers, occupational pension funds and investment funds stand between 10.9% and 21.5%, depending on the sector. Although sizeable, the impact of these losses on financial institutions’ capital is expected to be mitigated by factors such as banks’ income, insurers’ and occupational pension funds’ liabilities, and cash holdings by investment funds that were not included in the assessment.